Purpose

To evaluate the cost paid by patients in the United States for their branded, prescription medication, and the factors that determine the cost.

Design

Evaluation of publicly available information on the U.S. pharmaceutical distribution system.

Methods

Review of public information and interpretation based on the author’s experience.

Results

The price paid for branded, prescription medication by an insured patient is set by the patient’s insurance company—not the manufacturer, distributor, or pharmacy—and is typically a co-pay, which is a fraction of the wholesale acquisition cost (WAC). On the other hand, for an uninsured patient, the patient cost is higher than the WAC and may vary dramatically, depending on the pharmacy. Furthermore, lowering of the WAC by the manufacturer (eg, a new product in the same class) may not lower the patient payment, as that cost is set by the insurer and may depend on rebates from the manufacturer to the distributor and to the insurer. The proportion of patients in the United States covered by insurance is growing.

Conclusion

In the same way that the mean (or median) may not accurately describe a bimodal population, the WAC does not accurately describe the cost of branded, prescription medication to patients. To reduce medication costs to patients, recommendations are as follows: (1) selection of insurance plans whose formularies cover their medications in a low tier (eg, “Preferred”), (2) for patients without insurance, price compare at multiple pharmacies; (3) use manufacturer-supplied coupons to reduce out-of-pocket costs, and (4) consider therapeutics—optimal use of medications often executable with little or no cost to the patient.

The cost and quality of health care in the United States is a matter of public policy that impacts many sectors. In particular, the pricing of pharmaceuticals, while only 10% of the total health care cost, is of particular concern—probably owing, at least in part, to the visibility of these costs (ie, patient out-of-pocket cost). These costs (and ultimately who is paying for what) have been the subject of much discussion and some confusion. Payment for pharmaceuticals in the United States is a complex, interactive, nonintuitive process. With changes to public policy being discussed, I thought it might be useful to present the payment system in the United States for pharmaceutical products dispensed to the patient. The focus of this article is what the patient pays.

The most important determinant of how much a patient pays for his or her medication is whether the patient has prescription insurance coverage. A 2015 survey conducted by Consumer Reports found that one-third of Americans regularly take at least 1 prescription drug, and that 96% of these users of pharmaceuticals are covered by prescription insurance. The proportion of payment for outpatient prescription drug expenditures paid for by patients (in contrast to public funds or insurance) decreased from 26% in 2003 to 17% in 2013, and is estimated to decrease to 12% by 2023. While substantial differences exist in types of prescription coverage and individual plan benefits, I will first explore in some detail the process that determines how much an insured patient pays.

Insured Patients’ Flow of Payments

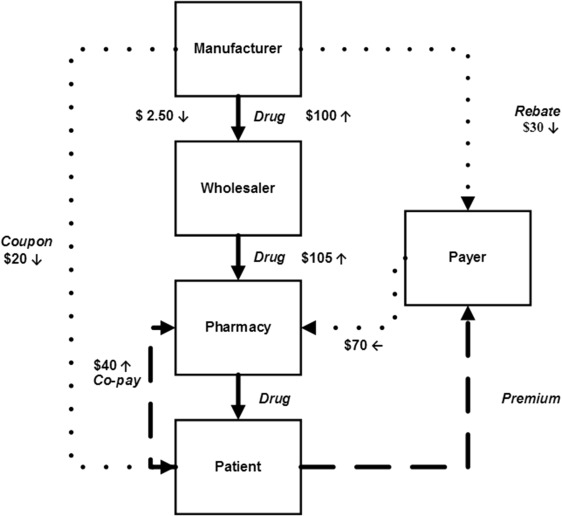

Shown in the Figure is a flow chart of payments for an example of a branded, pharmacy-dispensed drug for a patient with private insurance with a nominal price of US$100. In diseases for which multiple drugs are available as treatment, the manufacturer first negotiates with insurance companies/payers to secure a position on a formulary. This position determines the patient’s co-pay (out-of-pocket cost) and whether the drug will be placed in 1 of 3 categories: “Preferred” (lowest co-pay), “Nonpreferred” (covered without restrictions; eg, reimbursed without restrictions such as prior authorizations), or “Covered with restrictions.” To secure a preferred position on the formulary for a drug, a manufacturer will agree to rebate a portion of the drug cost to the payer/insurance company based on the competitiveness of the market. These rebates commonly range from 10% to 50%+ of the drug price.

In the example shown, the manufacturer has contracted for a preferred position on a formulary in a moderately competitive market and has agreed to rebate 30% of the price back to the payer/insurance company. The manufacturer then sells a 1-month supply of the product for $100 to the distributor (in this case, $100 is the wholesale acquisition cost [WAC]). The manufacturer also provides a negotiated distribution fee to the distributor (eg, 2.5%), as well as a guarantee that any product that expires at the distributor may be returned for a full refund. The wholesaler sells the product to the pharmacy at a marked-up price (eg, 5% mark-up, or $105). The pharmacy dispenses the product to the patient for the co-pay set by the patient’s insurance company (eg, $40) plus an agreed-upon amount from the payer/insurance company (eg, $70). Thus, the net profit for the pharmacy is $5. The manufacturer may also provide the patient with a coupon (in this example, for $20). While much attention has been given to claims that discounts have been given to a pharmacy from a manufacturer, this will have no impact on the co-pay for an insured patient.

Patients also pay an insurance premium, which may cover not only medications but also physicians and hospitals—which is difficult for us to assign to just this 1 drug. Payers receive that premium, and in this simple example of a single drug, assignment of a portion of that premium to this single drug is difficult to assign as well.

The cash flow for the system as shown in the Figure is summarized in the Table . For a drug with a nominal WAC of $100, the net revenue to the manufacturer is $67.50, and the net cost to the patient is $40 (not counting the insurance premium, or a possible discount coupon). For patients whose prescriptions are paid for in whole or in part by a federal health care program (including Medicare Part D insurance) it is illegal to use coupons to reduce a patient’s out-of-pocket expense. Recently, one pharmaceutical company recommended to the U.S. House Committee on Oversight and Government Reform to remove this restriction.

| Participant | Components | Net | Comment |

|---|---|---|---|

| Manufacturer | $100.00 − 2.50 − 30.00 | $67.50 | Not counting coupon |

| Patient | ($40.00) | ($40.00) | Not counting insurance premium (outflow) or coupon (income) |

| Wholesaler | $(100.00) + $2.50 + 105.00 | $7.50 | — |

| Pharmacy | ($105.00) + 40.00 + 70.00 | $5.00 | — |

| Payer | $(70.00) + 30.00 | $(40.00) | Not counting insurance premium (income) |

Stay updated, free articles. Join our Telegram channel

Full access? Get Clinical Tree